Chapter 7 vs Chapter 13: Which Bankruptcy Is Right for You in 2026?

Choosing the wrong bankruptcy chapter can mean years of unnecessary payments — or losing assets you could have protected. This guide explains every key difference between Chapter 7 and Chapter 13 so you can make the right decision for your situation.

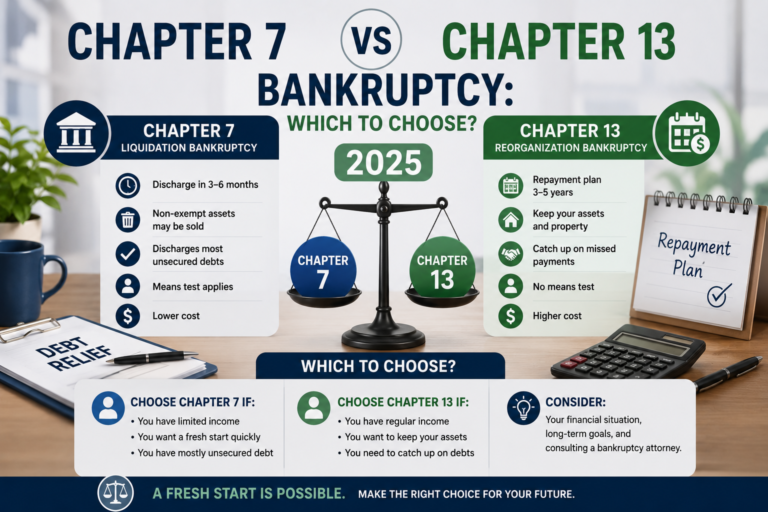

Chapter 7: The Fresh Start

Chapter 7 discharges most unsecured debts (credit cards, medical bills, personal loans) in 4–6 months. A trustee reviews assets — but 95% of filers have no non-exempt assets and keep everything they own. Requires passing the means test. Cannot have filed Chapter 7 within last 8 years.

Chapter 13: The Reorganization

Chapter 13 lets you keep all assets while repaying some or all debts through a court-supervised 3–5 year plan. Key advantage: allows you to catch up on mortgage arrears while keeping your home — something Chapter 7 cannot do. Requires regular income sufficient to fund the repayment plan.

Side-by-Side Comparison

| Factor | Chapter 7 | Chapter 13 |

|---|---|---|

| Duration | 4–6 months | 3–5 years |

| Income test | Must pass means test | Need steady income |

| Asset risk | Non-exempt at risk | All assets protected |

| Save home from foreclosure | Temporary stop only | ✅ Yes |

| Credit report | 10 years | 7 years |

| Attorney fees (typical) | $1,000–$2,000 | $3,000–$5,000 |

5 Situations That Determine Your Choice

1. Behind on mortgage, want to keep home → Chapter 13

Chapter 13 allows you to spread mortgage arrears over your 3–5 year plan while keeping your home. Chapter 7 only provides a temporary automatic stay — foreclosure resumes after.

2. Income above state median → Chapter 13

If you don’t pass the Chapter 7 means test, you’re directed to Chapter 13. See our bankruptcy means test guide.

3. Significant non-exempt assets → Chapter 13

Chapter 7 puts non-exempt property at risk of liquidation. Chapter 13 lets you keep everything in exchange for paying creditors the value of those assets through your plan.

4. Mostly credit card/medical debt, modest income, few assets → Chapter 7

Classic Chapter 7 scenario. See our complete Chapter 7 DIY guide.

5. Prior Chapter 7 within last 8 years → Chapter 13

Cannot refile Chapter 7 within 8 years of a prior discharge. Chapter 13 available after 4 years from prior Chapter 7.

FAQ

Which is worse for credit?

Chapter 7 stays 10 years vs 7 for Chapter 13. But Chapter 13 takes 3–5 years to complete, delaying your credit rebuilding. Long-term impact is often similar.

What if I can’t complete Chapter 13?

You can convert to Chapter 7 (if eligible), request hardship discharge, or have the case dismissed — leaving original debts intact. Understand this risk before choosing Chapter 13.

Free Chapter Comparison Worksheet

10 questions to find which bankruptcy chapter fits your situation.