Considering Bankruptcy? Read This Before You Decide Anything

Bankruptcy carries a stigma that is wildly disproportionate to what it actually is — a legal process designed specifically to give people who are overwhelmed by debt a structured path forward. It is not a personal failure. It is a legal tool that exists because society has recognized that sometimes debt becomes impossible to manage and destroying people financially forever serves no one.

That said, it is a serious decision with real consequences that lasts years on your credit report and affects your financial options in that period. Before you file, before you even consult an attorney, there are things you need to think through honestly. This is that guide.

Disclaimer: This is educational information. Bankruptcy law is complex and state-specific. Consult a qualified bankruptcy attorney before making any decisions.

The First Question — Is Your Situation Actually Unmanageable?

Bankruptcy is the right answer for some situations and completely the wrong answer for others. Before evaluating bankruptcy, you need an honest assessment of whether your debt is truly unmanageable or whether it is very difficult but potentially workable with aggressive strategies.

Signals that suggest bankruptcy deserves serious consideration: your total unsecured debt exceeds your annual income. You are more than 90 days behind on multiple debts. You are receiving collection calls and wage garnishment is a real possibility. You have already tried budgeting, cutting expenses, and increasing income without making meaningful progress. You are using one debt to pay another — borrowing to make minimum payments — creating a spiral with no exit.

Signals that suggest bankruptcy may not be the right answer yet: your debt is high but your income is also growing. Your primary debt problem is student loans which are generally not dischargeable. Your financial difficulty is temporary rather than structural. You have non-exempt assets you would lose in Chapter 7 that matter to you.

What Bankruptcy Actually Does — And Does Not Do

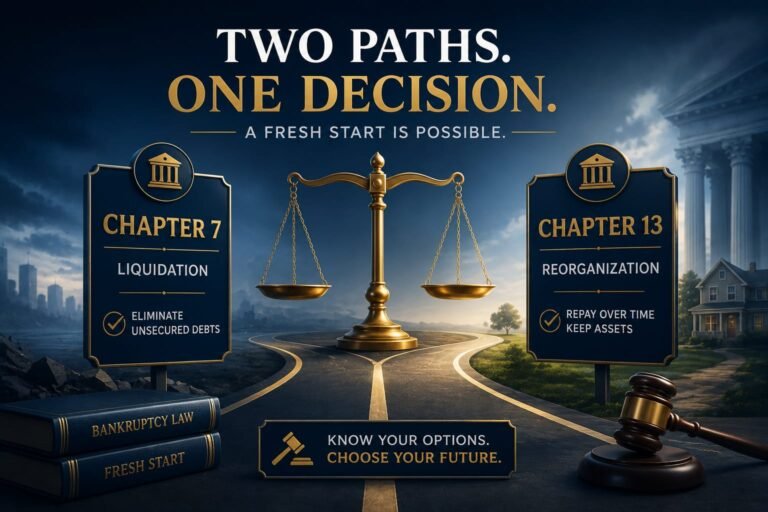

Chapter 7 bankruptcy eliminates most unsecured debts — credit cards, medical bills, personal loans, some older tax debts — through a process that typically takes 4 to 6 months. You keep exempt property which in most cases includes all of your furniture, clothing, retirement accounts, and often your home and car if you are current on those payments. The trade is that the bankruptcy stays on your credit report for 10 years.

Chapter 13 bankruptcy lets you keep all your property while repaying some or all of your debts through a 3 to 5 year repayment plan based on your disposable income. It stays on your credit report for 7 years and is often chosen by people with significant home equity they want to protect or income too high to qualify for Chapter 7.

What bankruptcy does not do: eliminate student loans in most cases, eliminate child support or alimony, eliminate recent tax debts, eliminate debts obtained through fraud, or eliminate secured debts if you want to keep the collateral.

The Credit Score Reality — Honest and Not as Bad as You Think

Yes, bankruptcy significantly damages your credit score. But here is what most people do not consider: if you are already months behind on multiple debts, your credit score is already severely damaged. The bankruptcy often does not reduce it much further from where it already is after serious delinquency. What it does is stop the ongoing damage and give you a clean baseline to rebuild from.

People with bankruptcy history commonly get secured credit cards within 12 months, car loans within 18 to 24 months at higher rates initially, and mortgages within 2 to 4 years for FHA loans. The credit impact is real and it lasts years, but it is not permanent and it does not prevent you from participating in credit markets — it just changes your terms temporarily.

Alternatives Worth Honestly Evaluating First

Bankruptcy should generally be a last resort after genuinely exploring alternatives. Debt negotiation and settlement — creditors accepting less than the full balance as payment in full — is possible and common for unsecured debts, though it has its own credit consequences and potential tax implications. Nonprofit credit counseling can negotiate interest rate reductions through formal debt management plans. Talking directly to creditors about hardship programs provides temporary relief in some cases.

The honest question to ask about alternatives: is this a bridge to a realistic resolution or am I just extending a situation that is not actually resolvable without bankruptcy? Alternatives make sense when there is a genuine path through. They are delay rather than solution when the debt is structurally unmanageable.

The Emotional Reality Nobody Talks About

Filing bankruptcy is emotionally difficult in ways that are hard to anticipate. There is a sense of failure that exists even when you intellectually know the decision is rational. There are practical challenges — the means test, the creditors meeting, the process of listing every debt you owe to every person and company you owe it to.

On the other side: people who have gone through bankruptcy describe an emotional relief that is almost physical. The constant background anxiety of unsustainable debt is gone. You can answer the phone again. You can think about something other than money for the first time in years. The fresh start is real, not just financial.

Before You Consult an Attorney — Prepare This

A bankruptcy consultation will be most useful if you arrive with a clear picture of your finances. Make a list of every debt: creditor name, current balance, interest rate, whether it is secured or unsecured, and how far behind you are. Know your monthly income after taxes. Know your monthly essential expenses. Know what assets you own and approximately what they are worth. This preparation helps the attorney give you accurate advice quickly and saves both time and money.

Frequently Asked Questions

Will I lose my house if I file bankruptcy? Usually not, if you are current on your mortgage payments and your home equity is within your state’s homestead exemption. Your bankruptcy attorney will calculate this specifically for your situation.

Will my employer find out I filed bankruptcy? Bankruptcy is a public record but employers do not typically search bankruptcy filings. Some employers with financial responsibility positions conduct credit checks where bankruptcy would appear.

Can I file bankruptcy more than once? Yes, with waiting periods. After Chapter 7 you must wait 8 years to file Chapter 7 again. The waiting periods vary depending on which chapter you filed previously.

What debts will bankruptcy not eliminate? Student loans in most cases, child support and alimony, recent tax debts, debts from fraud, and criminal restitution orders all survive bankruptcy.

Conclusion

Bankruptcy is not the end of your financial life — it is, for the right situations, the most direct path to beginning again from a sustainable position. The question is whether your situation is the right one for it. Be honest about whether alternatives are realistic for you. Understand what bankruptcy does and does not eliminate. Consult an attorney who practices bankruptcy law regularly. And if the answer is yes — give yourself permission to use the legal tool that exists precisely for situations like yours.