How to File Chapter 7 Bankruptcy Yourself in 2026: DIY Step-by-Step Guide

How to File Chapter 7 Bankruptcy Yourself in 2026: DIY Step-by-Step Guide

When debt becomes overwhelming and there is no realistic path to paying it off, bankruptcy can provide a genuine fresh start. Chapter 7 bankruptcy eliminates most unsecured debt — credit cards, medical bills, personal loans — and gives you a legal clean slate to rebuild your financial life.

While hiring a bankruptcy attorney is always recommended for complex cases, it is entirely legal to file Chapter 7 bankruptcy yourself, a process known as filing “pro se.” This DIY guide walks you through every step of the process so you can understand what is involved and make an informed decision about how to proceed.

Important disclaimer: This guide is for educational purposes. Bankruptcy law is complex and mistakes can have serious consequences. Consulting with a bankruptcy attorney — even for a free initial consultation — is strongly recommended before filing.

What Is Chapter 7 Bankruptcy?

Chapter 7 bankruptcy, often called “liquidation bankruptcy,” is the most common form of personal bankruptcy. In Chapter 7, a court-appointed trustee reviews your assets and may sell non-exempt assets to pay creditors. Most Chapter 7 filers have few or no non-exempt assets, meaning they complete the process without losing any property.

In exchange, most unsecured debts are discharged — legally eliminated. The entire process typically takes 4 to 6 months from filing to discharge. After discharge, creditors can no longer legally pursue you for those debts.

Debts that cannot be discharged in Chapter 7 include most student loans, recent taxes (generally less than 3 years old), child support and alimony, debts from fraud, and recent luxury purchases and cash advances (made within 90 days of filing).

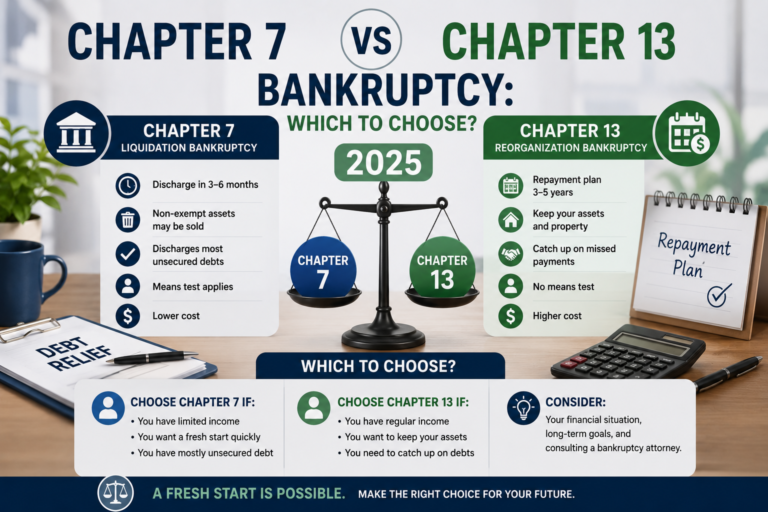

Chapter 7 vs. Chapter 13 Bankruptcy

Chapter 7 eliminates debt quickly but requires passing an income test. Chapter 13 is a repayment plan over 3 to 5 years and does not have the same income restrictions. Chapter 13 may be preferable if you want to save a home from foreclosure, have a significant amount of non-exempt assets you want to keep, or earn too much to qualify for Chapter 7. This guide focuses on Chapter 7.

Step 1: Determine If You Qualify — The Means Test

To file Chapter 7 bankruptcy, you must pass the “means test,” which evaluates whether your income is low enough to qualify. The means test was designed to prevent high-income filers from using Chapter 7 to discharge debts they could afford to repay.

The means test has two parts. First, compare your average monthly income over the past 6 months to the median income for your state and family size. If your income is at or below the median, you automatically qualify and do not need to complete the second part. If your income is above the median, you must complete a more detailed calculation that accounts for allowed expenses to determine if you have enough “disposable income” to repay debts. If your disposable income is below a certain threshold, you still qualify for Chapter 7.

The official means test form is Official Form 122A-1. Current median income figures by state are updated regularly and available on the US Trustee Program website (justice.gov/ust).

Step 2: Complete the Required Credit Counseling

Before filing bankruptcy, you are legally required to complete a credit counseling course from a government-approved agency. This course must be completed within 180 days before filing and takes about 60 to 90 minutes. The cost is typically $15 to $50, and fee waivers are available if you cannot afford it.

Find approved agencies at the US Trustee Program website. After completing the course, you will receive a certificate that must be filed with your bankruptcy petition.

Step 3: Gather Required Documents

Preparing your bankruptcy petition requires extensive documentation. Gather everything before you start filling out forms:

Tax returns for the past 2 years. Pay stubs and income documentation for the past 6 months. Bank statements for the past 6 months. All credit card and loan statements. Any mortgage or auto loan statements. Documentation of all assets: real estate, vehicles, retirement accounts, investments. Documentation of monthly expenses. Any lawsuits or judgments against you. List of all creditors with names, addresses, and account numbers.

Step 4: Complete the Bankruptcy Petition and Schedules

The bankruptcy petition is a set of official forms that disclose everything about your financial situation. The core documents include:

Form B101: Voluntary Petition — basic identifying information about you and your bankruptcy.

Schedule A/B: Lists all your property and assets, including everything you own regardless of value.

Schedule C: Claims exemptions for property you want to protect from the trustee.

Schedule D: Lists secured creditors (mortgages, car loans).

Schedule E/F: Lists unsecured priority creditors (taxes, child support) and general unsecured creditors (credit cards, medical bills).

Schedule G: Unexpired leases and executory contracts.

Schedule H: Co-debtors.

Schedule I: Current monthly income.

Schedule J: Current monthly expenses.

Form 106Dec: Declaration of accuracy — you sign under penalty of perjury that everything is accurate and complete.

Statement of Financial Affairs (Form 107): Detailed questions about recent financial activity including recent payments to creditors, property transfers in the past 2 years, and recent lawsuits.

All official bankruptcy forms are available for free at uscourts.gov/forms/bankruptcy-forms. Be extremely thorough and accurate. Omitting assets or creditors — even accidentally — can result in denial of discharge or criminal fraud charges.

Step 5: Understand Bankruptcy Exemptions

Exemptions are the legal protections that allow you to keep certain property in bankruptcy. What you can exempt varies significantly by state. Some states require you to use federal exemptions; others let you choose between state and federal exemptions.

Common exemptions include: homestead exemption (protects equity in your primary home, ranging from $25,000 to unlimited depending on state), vehicle exemption (typically $2,500 to $5,000), retirement accounts (most are 100% exempt), personal property exemptions for furniture, clothing, tools of trade, and wildcard exemption (can be applied to any property).

Research your specific state’s exemptions carefully. If you own significant assets, maximizing your exemptions is one of the most important aspects of bankruptcy planning. This is a key area where consulting an attorney adds significant value.

Step 6: File Your Petition

File your completed bankruptcy petition at your local US Bankruptcy Court. Find the correct court at uscourts.gov. You can file in person or, in many districts, electronically. The filing fee for Chapter 7 is $338. Fee waivers are available if your income is below 150% of the federal poverty guidelines; fee installments are also available.

When you file, you will receive a case number and the automatic stay immediately goes into effect. The automatic stay is a powerful legal protection that immediately stops most collection actions — creditor calls, lawsuits, wage garnishments, foreclosures, and repossessions — the moment you file.

Step 7: The 341 Meeting of Creditors

Approximately 21 to 40 days after filing, you must attend a Meeting of Creditors, also called a 341 meeting. Despite the name, creditors rarely attend. The trustee assigned to your case will ask you questions under oath to verify the accuracy of your petition.

Typical questions include verifying your identity, confirming you reviewed your petition for accuracy, asking about any assets not disclosed, and verifying recent financial transactions. The meeting is usually brief — often just 5 to 10 minutes. Bring your photo ID and Social Security card.

Step 8: Complete the Debtor Education Course

After filing but before receiving your discharge, you must complete a second required course — a debtor education or financial management course. Like the pre-filing credit counseling, this must be from an approved agency and typically costs $15 to $50. File the completion certificate with the court.

Step 9: Receive Your Discharge

If no creditors object and the trustee finds no issues with your petition, you will receive your discharge order approximately 60 to 90 days after the 341 meeting. The discharge order legally eliminates the dischargeable debts listed in your petition. Creditors are legally prohibited from ever trying to collect these debts again.

Life After Bankruptcy: Rebuilding Your Credit

A Chapter 7 bankruptcy remains on your credit report for 10 years, but its impact on your credit score diminishes over time. Many people find that their credit scores actually improve in the years following bankruptcy as they eliminate debt and establish positive payment history.

Start rebuilding immediately: get a secured credit card, pay it in full every month, become an authorized user on someone else’s account, and monitor your credit report regularly. Many people achieve credit scores in the 650 to 700 range within 2 to 3 years of their bankruptcy discharge.

When to Hire a Bankruptcy Attorney

Consider hiring an attorney if you own significant non-exempt assets, have recently transferred property or paid large amounts to creditors, are behind on mortgage payments and want to keep your home, have complex income sources, or have previously filed bankruptcy. Bankruptcy attorneys typically charge $1,000 to $3,500 for Chapter 7 cases. Some offer free initial consultations. The National Association of Consumer Bankruptcy Attorneys (nacba.org) provides a directory of members.