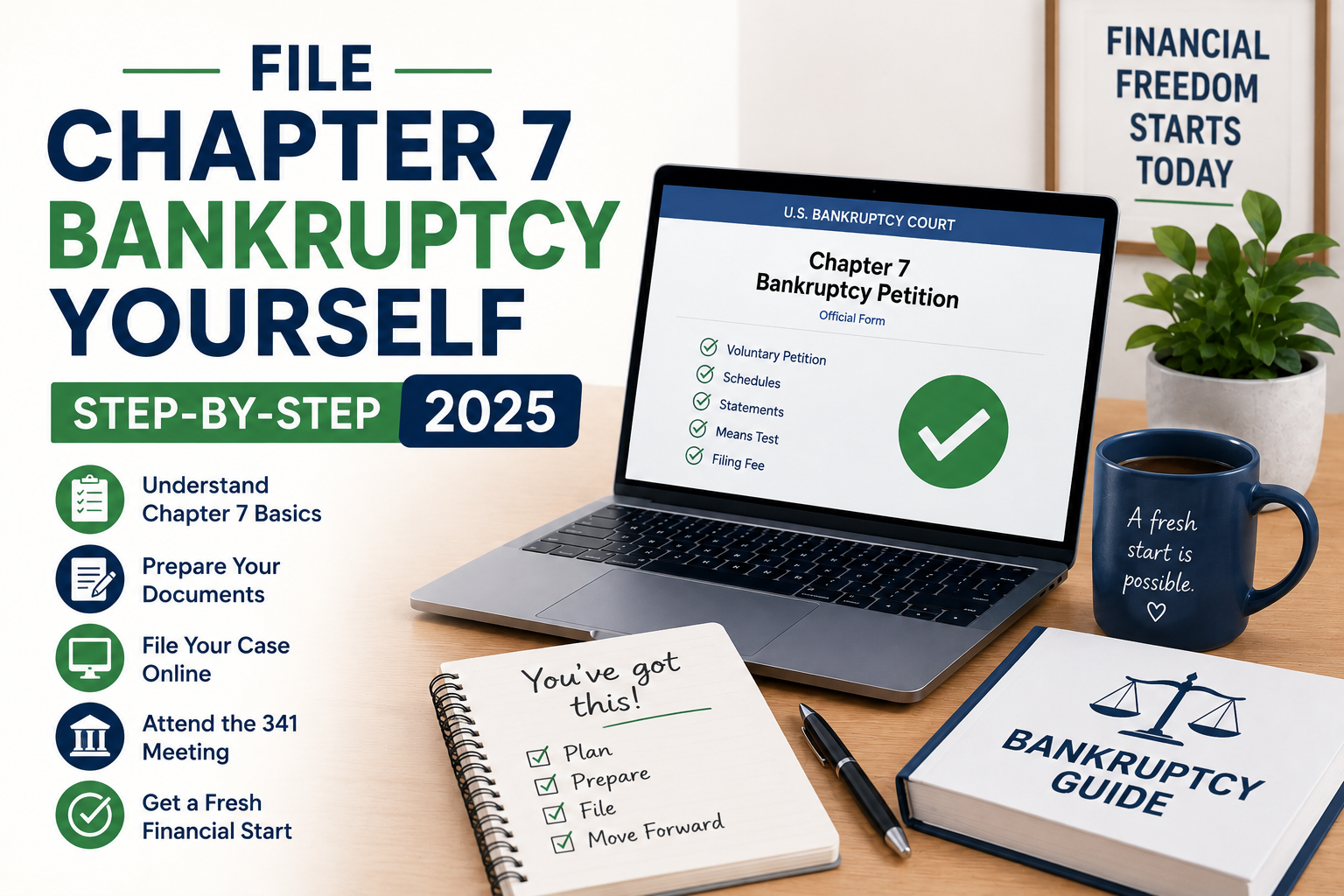

File Chapter 7 Bankruptcy Yourself: Step-by-Step 2025

$1,738 — Average attorney fee for Chapter 7 in 2024 — DIY saves this entire amount

$338 — Federal court filing fee for Chapter 7 (waivable for low-income filers)

3–6 mo — Typical time from filing to discharge for straightforward Chapter 7 cases

96% — Chapter 7 cases resulting in discharge when properly filed (USCOURTS 2024)

$0 — Cost of official bankruptcy petition forms (free at uscourts.gov)

Can You Really File Chapter 7 Without a Lawyer?

Yes — and thousands of people do it every year. Filing bankruptcy without an attorney is called filing ‘pro se’ (representing yourself), and federal courts must accept pro se filings. The average attorney fee for Chapter 7 is $1,738 (2024 National Bankruptcy Forum survey). The court filing fee is $338, waivable if your income is below 150% of the federal poverty line. Total DIY cost: $338 or free.

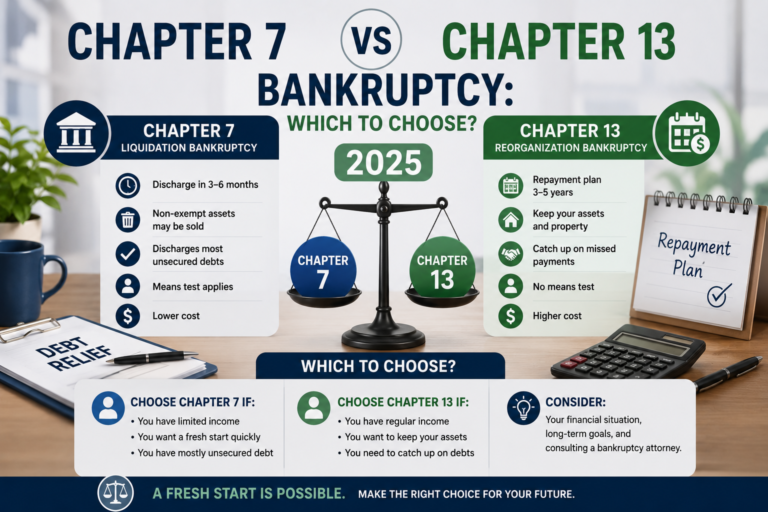

Chapter 7 is a liquidation bankruptcy that discharges most unsecured debt (credit cards, medical bills, personal loans) in 3–6 months. You don’t make payments to creditors — eligible debts are legally eliminated. Here’s the complete process.

Step 1: Confirm You Qualify with the Means Test

The means test determines if your income is low enough for Chapter 7. Calculate your average monthly income over the 6 months before filing. If annualized, it’s below your state’s median income for your household size — you automatically qualify. Use free calculators at legalconsumer.com/bankruptcy. Social Security income is completely excluded from this calculation — a critical exemption many people miss.

Step 2: Gather All Financial Documents

You’ll need: 6 months of pay stubs or income proof, last 2 years of tax returns, last 3 months of bank statements, complete creditor list with balances and account numbers, list of all assets with current values, vehicle titles, mortgage and auto loan statements. Create a spreadsheet listing every single debt — this becomes your creditor matrix for the bankruptcy schedules.

Step 3: Complete the Required Bankruptcy Forms

All official forms are free at uscourts.gov/forms/bankruptcy-forms. Key forms required for Chapter 7:

| Form | What It Covers |

|---|---|

| Voluntary Petition (B101) | Basic identifying information and case type selection |

| Schedule A/B | All property and assets you currently own |

| Schedule C | Property you’re claiming as legally exempt (protected) |

| Schedule D/E/F | All secured, priority, and unsecured debts owed |

| Means Test (B122A) | Income calculation to qualify for Chapter 7 |

| Statement of Financial Affairs | Financial history: sales, payments, lawsuits in past 2 years |

Step 4: File With Your Local Bankruptcy Court

Find your federal bankruptcy district at uscourts.gov/court-locator. File in person (bring 3 copies of everything) or electronically if your district allows pro se electronic filing. Pay the $338 fee or submit fee waiver Form B103B. Upon filing, an automatic stay immediately stops all collection calls, lawsuits, wage garnishments, and foreclosures. The stay takes effect the moment you file, before any court processing.

Step 5: The 341 Meeting of Creditors

About 30 days after filing, you attend a 341 meeting with a bankruptcy trustee — not a judge. This typically lasts 5–10 minutes. The trustee verifies your identity and confirms your filing’s accuracy. Bring photo ID and proof of Social Security number. Answer questions truthfully and concisely. Creditors rarely attend in straightforward Chapter 7 cases.

For the comparison between types: Chapter 7 vs Chapter 13: Which Should You Choose? | For income qualification: The Bankruptcy Means Test: Complete Guide 2025

Frequently Asked Questions

What debts are NOT discharged in Chapter 7?

Non-dischargeable debts include: student loans (in most cases), taxes owed within 3 years, child support and alimony, debts from fraud or intentional harm, and criminal fines. All other debts — credit cards, medical bills, personal loans, collection accounts — are typically fully discharged.

Will I lose my house or car in Chapter 7?

Not necessarily. Most states have homestead exemptions protecting home equity up to a set amount. For cars, most states protect $2,400–$50,000 in equity depending on the state. You can also ‘reaffirm’ a secured debt (agreeing to keep paying) to retain the asset.

How long does Chapter 7 stay on my credit report?

10 years from filing date. However, many people begin rebuilding credit within 1–2 years post-discharge through secured credit cards and responsible use. The impact on credit scores diminishes significantly after 2–3 years.

Can I file Chapter 7 if I filed bankruptcy before?

Yes, with waiting periods: 8 years after a previous Chapter 7 discharge; 4 years after a Chapter 13 discharge. The clock starts from filing date to filing date, not discharge to filing.

Should I use bankruptcy filing software?

For complex cases, yes — BankruptcyPro ($100–$150) and Best Case ($400+) help with form completion. For simple cases with few assets and straightforward unsecured debts, the free official forms with careful attention to detail are completely sufficient.

How long does the whole process take from start to finish?

From filing to discharge: typically 4–6 months for straightforward Chapter 7 cases. If the trustee raises no objections after your 341 meeting, you receive your discharge order approximately 60–90 days after that meeting.

After Filing: The Finish Line

After your 341 meeting, assuming no complications, your discharge arrives 60–90 days later. The discharge order legally eliminates all qualifying debts included in your filing. You’re debt-free. Total DIY cost: $338. Total debt eliminated: potentially tens of thousands of dollars. That ratio is hard to beat.