How to File Bankruptcy Without a Lawyer: Is Pro Se Filing Possible and When to Try It

Filing for bankruptcy without an attorney — called pro se filing — is legally permitted in federal bankruptcy courts. People successfully file bankruptcy without lawyers every day. However, the bankruptcy code is complex, the paperwork requirements are extensive, and mistakes can have serious consequences including dismissal of your case, loss of the automatic stay protection, or in serious cases, fraud allegations. This guide gives you an honest assessment of when pro se bankruptcy is feasible and what the process involves.

Disclaimer: This guide is for educational purposes only and does not constitute legal advice. Bankruptcy law is complex and the consequences of errors are significant. Consulting with a bankruptcy attorney before proceeding is strongly recommended.

The Honest Answer — When Pro Se Bankruptcy Is and Is Not Realistic

Pro se Chapter 7 bankruptcy is most feasible for people with a straightforward financial situation: primarily unsecured debt (credit cards, medical bills, personal loans), no significant non-exempt assets, no complex ownership interests in businesses or real estate, no recent unusual financial transactions that could be questioned, and sufficient time and organizational ability to handle extensive paperwork. Experienced bankruptcy attorneys often describe straightforward no-asset Chapter 7 cases as relatively formulaic — the same paperwork filled out the same way for most filers.

Pro se Chapter 13 is significantly more challenging and most bankruptcy professionals advise against it for non-attorneys. Chapter 13 involves proposing a complex multi-year repayment plan, navigating objections from creditors and trustees, and making strategic decisions about plan structure that have major long-term financial implications. The success rate for pro se Chapter 13 filings is substantially lower than attorney-represented cases.

For understanding whether Chapter 7 or Chapter 13 is right for your situation, see our guide on Chapter 7 vs Chapter 13 Bankruptcy.

Required Bankruptcy Documents — What You Need to File

A complete Chapter 7 bankruptcy filing requires a substantial set of documents and forms. The Voluntary Petition (Official Form 101) is the main filing document establishing your case. Schedules A through J cover your assets, liabilities, income, expenses, executory contracts, and co-debtors in extensive detail — each schedule requires careful, accurate completion. Statement of Financial Affairs (Official Form 107) requires a detailed history of financial transactions for the past two to four years. Statement of Intention describes what you intend to do with secured property. The Means Test Calculation (Official Form 122A-1) determines whether you qualify for Chapter 7 based on your income.

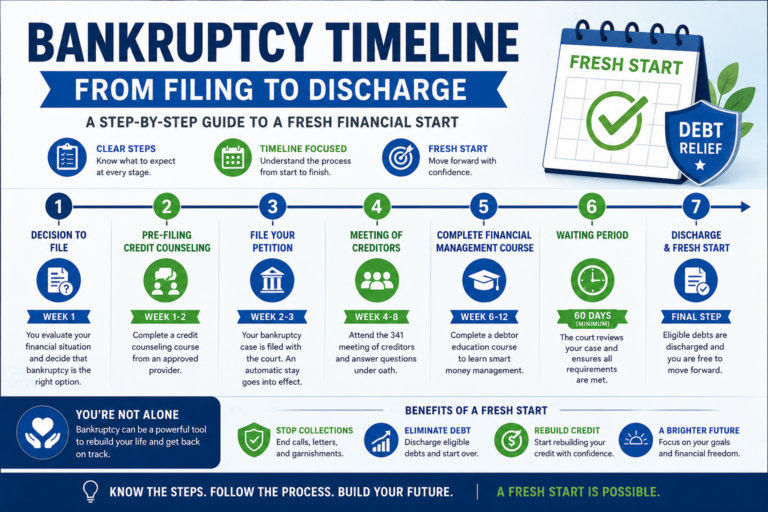

Prior to filing, you must complete a credit counseling course from an approved provider and obtain the certificate. After filing, you must complete a debtor education course and obtain that certificate before discharge.

Step by Step Pro Se Chapter 7 Filing Process

Step 1: Gather all financial documents. This includes tax returns for the past two to three years, pay stubs for the past six months, bank statements for the past year, a complete list of all debts with creditor names and balances, documentation of all assets and their approximate values, and any correspondence from creditors or collection agencies.

Step 2: Complete and obtain your credit counseling certificate from an approved provider (find approved providers at justice.gov/ust).

Step 3: Complete all required bankruptcy forms. The official forms are available free at uscourts.gov. Read the instructions for each form carefully. The schedules require complete and accurate disclosure of all assets and liabilities — incomplete disclosure is the most common source of serious problems in pro se cases.

Step 4: File your petition and all required forms with the bankruptcy court in your district. There is a filing fee of approximately $338 for Chapter 7. If you cannot afford the fee, you can apply for a fee waiver based on income.

Step 5: The automatic stay goes into effect immediately upon filing, stopping most collection actions. Read our guide on The Automatic Stay in Bankruptcy for what this protection covers.

Step 6: Approximately 30 to 45 days after filing, you attend the 341 Meeting of Creditors. The trustee asks you questions about your financial affairs under oath. Creditors can also attend and ask questions though most do not in no-asset cases.

Step 7: Complete your debtor education course within 60 days after the 341 meeting and file the certificate with the court.

Step 8: If no issues arise, your discharge is entered approximately 60 to 90 days after the 341 meeting, eliminating your eligible debts.

Common Pro Se Mistakes and How to Avoid Them

Incomplete or inaccurate asset disclosure is the most consequential pro se mistake. Failing to list assets, undervaluing assets, or omitting recent asset transfers can constitute bankruptcy fraud — a federal crime. List everything, even assets you believe are exempt.

Incorrect exemption selection can result in losing property you could have kept. If your state allows choosing between federal and state exemptions, calculate both systems carefully to determine which provides better protection for your specific assets.

Missing deadlines is a frequent pro se problem. Bankruptcy has numerous specific deadlines — the credit counseling certificate must predate filing, the debtor education certificate must be filed within a specific window. Calendar all deadlines when you file.

Not understanding the means test can result in filing a case you do not qualify for. The means test calculation is complex and errors can result in case dismissal.

Lower-Cost Alternatives to Full Pro Se Filing

If the cost of a bankruptcy attorney is the primary barrier, several alternatives provide professional assistance at reduced cost. Limited scope representation (also called unbundled legal services) allows you to hire an attorney for specific parts of the process — reviewing your paperwork, advising on exemptions, or appearing with you at the 341 meeting — rather than full representation. Legal aid organizations in most areas provide free or low-cost bankruptcy assistance to qualifying low-income individuals. Bankruptcy petition preparers can complete the paperwork under your direction for a fee, though they cannot provide legal advice.

Frequently Asked Questions About Pro Se Bankruptcy

How long does pro se Chapter 7 take? The timeline is the same as attorney-represented cases: filing to discharge typically takes 4 to 6 months for straightforward no-asset Chapter 7 cases.

Will the bankruptcy trustee help me if I am filing pro se? The trustee cannot provide legal advice but court staff can direct you to correct forms and explain procedures. The bankruptcy court’s website for your district typically has pro se filer resources.

Can I hire a lawyer later if I get into trouble filing pro se? Yes, you can retain an attorney at any point. However, correcting errors made in a pro se filing is more complex and expensive than doing it right the first time.

Conclusion

Pro se Chapter 7 bankruptcy is feasible for individuals with straightforward financial situations who are willing to invest significant time in understanding the process and completing paperwork carefully and completely. The cost savings can be meaningful — attorney fees for Chapter 7 typically range from $1,000 to $3,500. The risks are real and should not be minimized. For the best outcomes in most situations, at minimum a consultation with a bankruptcy attorney to evaluate your specific case is a worthwhile investment before deciding to file pro se. Also read our guides on Bankruptcy Exemptions and What Debts Cannot Be Discharged in Bankruptcy to fully understand what bankruptcy can and cannot do for your situation.