Life After Bankruptcy: Complete Recovery Guide

Filing for bankruptcy is one of the most difficult financial decisions a person can make. But the moment your debts are discharged, a new chapter begins. Life after bankruptcy can be rich, stable, and financially healthy — if you approach it with the right mindset and strategy. This is your complete guide to thriving after bankruptcy.

The Emotional Side of Bankruptcy Recovery

Before diving into practical steps, it is important to acknowledge something: bankruptcy often carries emotional weight. Many people feel shame, embarrassment, or a sense of failure after filing. These feelings are common and understandable. But here is the truth — bankruptcy is a legal tool. It exists because the law recognizes that people face impossible financial circumstances through job loss, medical crises, divorce, and other life events often beyond their control. Using the legal system to get relief is not a failure. It is resourcefulness.

Immediately After Discharge: First Steps

Pull your credit reports. Access your reports from Equifax, Experian, and TransUnion at AnnualCreditReport.com. Check that all discharged accounts are showing correctly and dispute any errors. Read How to Rebuild Credit After Bankruptcy for detailed guidance.

Create a bare-bones budget. Now that your debt burden is lifted, you have more cash flow. Build a realistic monthly budget covering all basic needs, including an emergency fund contribution.

Open a savings account. Even saving $25 to $50 per month creates a buffer that can prevent you from falling back into serious debt.

Keep all your bankruptcy documents. Store your discharge order and all bankruptcy paperwork safely. You may need them if creditors ever try to collect a discharged debt.

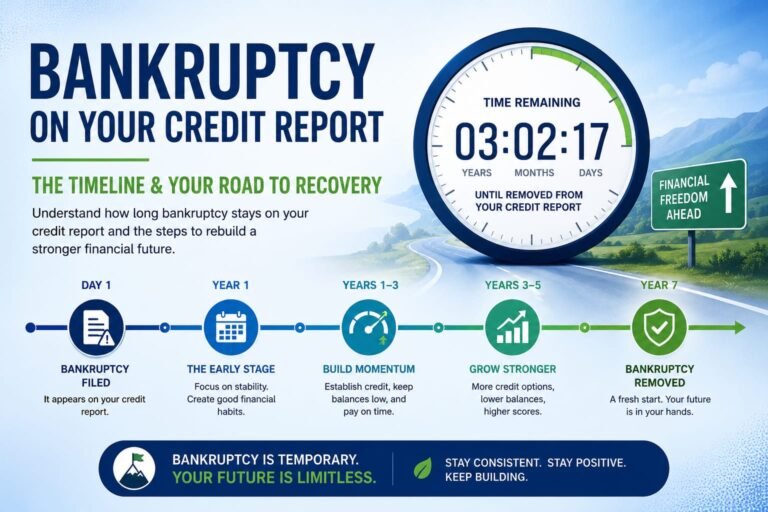

Credit Recovery Timeline

- Year 1: Stabilize, get a secured credit card, establish payment history

- Year 2: Score often reaches 620 to 660; auto loan eligibility improves

- Year 3: Many people qualify for FHA mortgages with responsible credit use

- Year 4-5: Score can reach 700+ with disciplined behavior

- Year 7 or 10: Bankruptcy removed from credit report entirely

Read How Long Does Bankruptcy Stay on Credit Report for the full timeline.

Build an Emergency Fund First

The number one reason people return to bankruptcy is the lack of an emergency fund. When an unexpected expense arises and there are no savings, people turn to credit cards and loans, restarting the debt cycle. After bankruptcy, make building an emergency fund your first financial priority. Start with a goal of $1,000, then grow to 3 to 6 months of living expenses in a separate savings account you do not touch except for true emergencies.

Renting After Bankruptcy

Many landlords will rent to you after bankruptcy, especially if you can show steady employment and sufficient income, a sincere explanation of what caused the bankruptcy, positive references from previous landlords, and a willingness to pay a larger security deposit. Look for individual landlords rather than large property management companies, as they tend to have more flexibility in screening.

Buying a Car After Bankruptcy

You can get an auto loan after bankruptcy, but expect higher interest rates initially. Wait at least 1 year after discharge if possible to give your score time to recover. Make a larger down payment, consider a reliable used car, get pre-approved before shopping, and refinance the loan after 12 to 18 months of on-time payments when your score has improved.

Buying a Home After Bankruptcy

Home ownership after bankruptcy is absolutely possible. FHA loans require a 2-year waiting period after Chapter 7 discharge (or 1 year into a Chapter 13 plan with court approval). VA loans for eligible veterans also require a 2-year wait after Chapter 7. Conventional loans require a 4-year waiting period after Chapter 7. During the waiting period, focus on rebuilding your credit and saving for a down payment.

Protecting Yourself From Future Financial Crises

- Get adequate insurance — Health, auto, renter’s or homeowner’s, and disability insurance protect against the unexpected expenses that cause bankruptcy.

- Avoid co-signing — After bankruptcy, you cannot afford to be responsible for someone else’s debt.

- Build multiple income streams — A single income is vulnerable. Look for freelancing or side income opportunities.

- Keep debt levels manageable — Never carry a balance on a credit card you cannot pay off at month’s end.

- Continue financial education — Read personal finance books and consider working with a nonprofit credit counselor.

Conclusion

Life after bankruptcy is not just survivable — it is an opportunity. The fresh start that bankruptcy provides gives you a foundation to build something stronger and more stable than what came before. With disciplined budgeting, strategic credit rebuilding, and a commitment to financial health, you can achieve genuine prosperity after bankruptcy.

Your past financial struggles do not define your future. What defines your future is what you do starting today. Take it one step at a time, celebrate small wins, and remember that millions of people have successfully rebuilt their financial lives after bankruptcy. The road ahead is wide open.