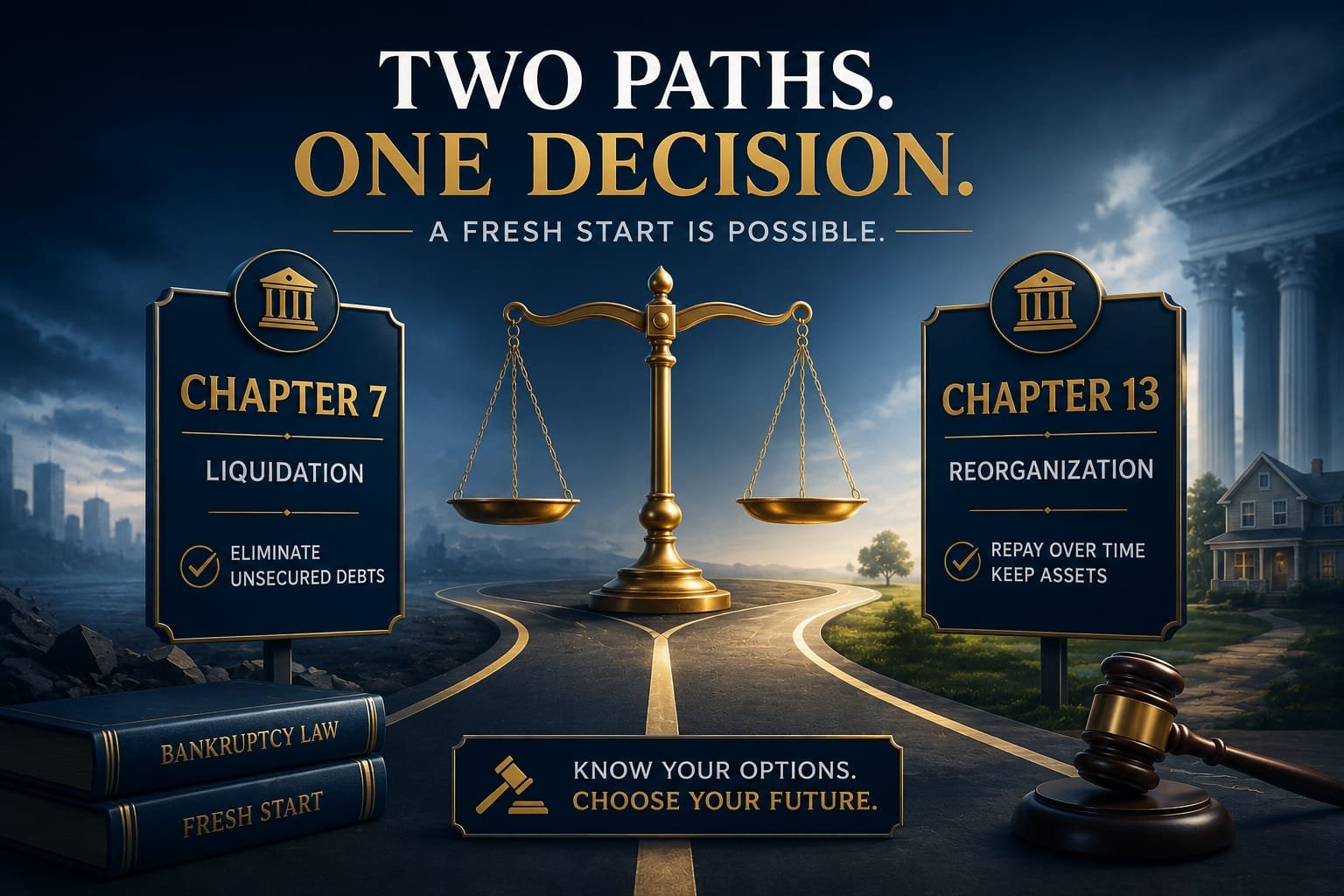

Chapter 7 vs Chapter 13 Bankruptcy: Which is Right for You?

Choosing between Chapter 7 and Chapter 13 bankruptcy is one of the most important financial decisions you can make. Both offer legal protection from creditors and a path to financial recovery, but they work very differently and suit different situations. This guide explains both options clearly so you can understand which may be appropriate for your circumstances.

Disclaimer: This is for educational purposes only. Always consult a qualified bankruptcy attorney for legal advice specific to your situation.

What is Chapter 7 Bankruptcy?

Chapter 7 is called liquidation bankruptcy. A bankruptcy trustee reviews your assets and may sell non-exempt property to pay creditors. Most unsecured debts — credit cards, medical bills, personal loans — are discharged, meaning legally eliminated, at the end of the process. Chapter 7 typically takes 3 to 6 months from filing to discharge. It is the fastest form of bankruptcy relief available.

What is Chapter 13 Bankruptcy?

Chapter 13 is called reorganization bankruptcy. Instead of liquidating assets, you propose a 3 to 5 year repayment plan to pay back some or all of your debts. You keep your assets including your home and car as long as you make the plan payments. At the end of the repayment period, remaining eligible debts are discharged.

Key Differences Between Chapter 7 and Chapter 13

Duration: Chapter 7 takes 3 to 6 months. Chapter 13 takes 3 to 5 years. Asset protection: Chapter 7 may require selling non-exempt assets. Chapter 13 lets you keep all assets if you complete the payment plan. Income requirements: Chapter 7 requires passing a means test — your income must be below your state median or you must pass a disposable income calculation. Chapter 13 requires sufficient regular income to fund a repayment plan. Home foreclosure: Chapter 13 allows you to catch up on mortgage arrears through the plan and save your home. Chapter 7 does not provide this mechanism.

Who Qualifies for Chapter 7?

To qualify for Chapter 7 you must pass the means test. If your income is below your state’s median income for your household size, you automatically qualify. If your income is above the median, you must complete a detailed calculation showing you do not have sufficient disposable income to fund a Chapter 13 plan. An attorney can run the means test for you.

Who Should Choose Chapter 13?

Chapter 13 is the better choice if you earn too much to qualify for Chapter 7, you are behind on mortgage payments and want to save your home, you have non-exempt assets you want to protect, you have debts that cannot be discharged in Chapter 7 such as certain tax debts that can be handled through a Chapter 13 plan, or you filed Chapter 7 within the past 8 years and are not eligible to file again.

Conclusion

Chapter 7 offers faster relief and complete discharge of most unsecured debts but may affect non-exempt assets and requires passing the means test. Chapter 13 takes longer but protects assets, saves homes from foreclosure, and is available to higher-income filers. The right choice depends entirely on your income, assets, debts, and goals. Consulting a bankruptcy attorney for a free initial consultation is the best first step toward making this decision.

===== ARTICLE 2 =====

TITLE: The Automatic Stay in Bankruptcy: How It Protects You Immediately

CATEGORY: LLC Basics

FOCUS KEYWORD: automatic stay bankruptcy

META DESCRIPTION: The automatic stay is one of bankruptcy’s most powerful protections, stopping collection calls, lawsuits, and foreclosures immediately upon filing. Learn how it works.

FEATURED IMAGE PROMPT: Shield blocking creditor calls and collection notices, automatic stay protection concept, strong blue and gold legal protection illustration, immediate relief theme

ARTICLE CONTENT:

One of the most immediate and powerful benefits of filing for bankruptcy is something called the automatic stay. The moment your bankruptcy petition is filed with the court, the automatic stay goes into effect — stopping most collection actions against you instantly. For people dealing with harassing collection calls, wage garnishment, or even foreclosure, the automatic stay provides immediate relief while the bankruptcy process proceeds.

Disclaimer: This content is for educational purposes only. Consult a bankruptcy attorney for advice specific to your situation.

What Does the Automatic Stay Stop?

The automatic stay immediately stops: collection calls and letters from creditors and collection agencies, lawsuits seeking money judgments, wage garnishments, bank account levies, foreclosure proceedings, eviction proceedings in many cases, utility service disconnections, and repossession of property. The breadth of the automatic stay protection is one of the primary reasons people file for bankruptcy even when they are uncertain about the full process.

How Long Does the Automatic Stay Last?

In a Chapter 7 case the automatic stay remains in effect until the bankruptcy is discharged, dismissed, or closed — typically 3 to 6 months. In a Chapter 13 case the stay lasts throughout the entire repayment plan period, providing years of protection. If a creditor wants to take action against you during the stay, they must ask the bankruptcy court for permission by filing a motion for relief from stay.

What the Automatic Stay Does NOT Stop

The automatic stay does not stop everything. It does not stop criminal proceedings, child support and alimony collection, certain tax audits and assessments, actions by government agencies to enforce police and regulatory powers, and evictions where a judgment was already entered before filing in some cases. Understanding these exceptions is important for setting realistic expectations.

What to Do If a Creditor Violates the Automatic Stay

If a creditor continues collection actions after your bankruptcy is filed, they are violating the automatic stay and may be liable for actual damages, attorney fees, and in some cases punitive damages. Notify your bankruptcy attorney immediately if any creditor contacts you after filing. Document every contact — date, time, creditor name, what was said or done.

Conclusion

The automatic stay is one of the most powerful immediate protections available in the American legal system. Filing bankruptcy stops collection calls, lawsuits, garnishments, and foreclosures instantly. Understanding how the stay works, how long it lasts, and what it does not cover helps you use this protection effectively during the bankruptcy process.