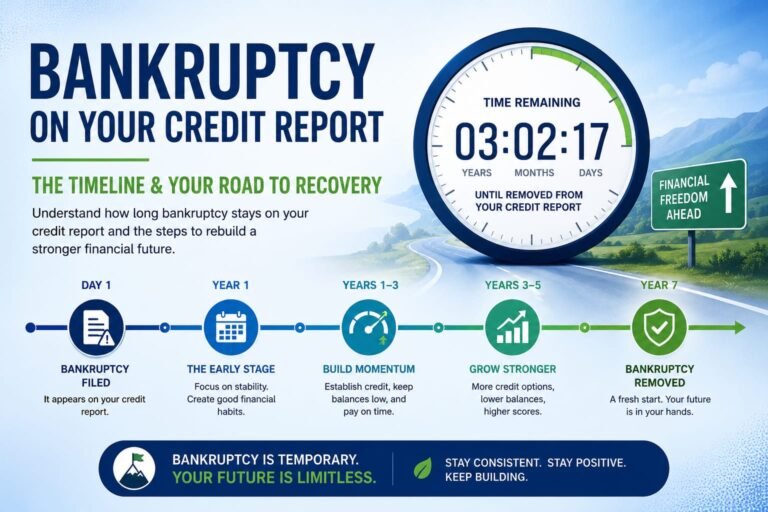

Post-Bankruptcy Recovery · diybankruptcyguide.com Life After Bankruptcy: How to Rebuild Credit and Finances in 2026

Bankruptcy is not a financial death sentence — it’s a legal reset. The fresh start it provides is real, and the path to solid financial footing after bankruptcy is well-documented. People rebuild from bankruptcy every day and go on to buy homes, drive reliable cars, and achieve financial security. This guide gives you the specific steps to rebuild your credit and finances starting from the day of discharge.

Immediately After Discharge: The Financial Foundation

Step 1: Verify Your Credit Reports Are Accurate

Within 30–60 days of discharge, pull all three credit reports (Equifax, Experian, TransUnion) at AnnualCreditReport.com. Verify that all discharged accounts show “discharged in bankruptcy” with a $0 balance — not “past due” or “in collections.” Errors in post-bankruptcy credit reporting are extremely common and can seriously impair rebuilding. Dispute any incorrect entries with each bureau.

Step 2: Open a Secured Credit Card

A secured credit card is the fastest credit rebuilding tool available immediately after bankruptcy. You deposit $200–$500 as collateral, and it becomes your credit limit. Use it for one or two small monthly purchases, pay the full balance every month, and the on-time payment history begins rebuilding your score immediately. Best secured cards for bankruptcy recovery: Discover it Secured, Capital One Platinum Secured, and OpenSky Secured Visa (no credit check).

Step 3: Open a Credit-Builder Loan

Credit-builder loans from credit unions and online lenders (Self, Kikoff) are designed specifically for credit rebuilding. You make monthly payments into a savings account — the money becomes yours at the end. The on-time payments are reported to credit bureaus, building credit history while simultaneously building savings. A $35/month credit-builder loan adds both payment history and savings over 24 months.

Step 4: Rebuild Emergency Savings

Before aggressively rebuilding credit, establish a $1,000–$2,000 emergency fund in a high-yield savings account. This prevents the small unexpected expenses that triggered pre-bankruptcy financial stress from immediately derailing your fresh start. Aim to grow this to 3–6 months of living expenses over 12–24 months.

6–12 Months Post-Discharge

Monitor Your Credit Score Monthly

Use free credit monitoring through your bank, Credit Karma, or Chase Credit Journey. Track your progress monthly. A typical trajectory: discharge → 500–550 score → 580–620 at 6 months → 640–680 at 12 months — with consistent positive credit behavior.

Add an Installment Loan

Having both revolving credit (credit card) and installment credit (loan with fixed payments) strengthens your credit profile. A credit-builder loan, small personal loan, or even a car loan (if you need one) adds installment credit variety.

Become an Authorized User

Ask a family member or close friend with excellent credit to add you as an authorized user on their credit card. Their positive account history can appear on your credit report, providing a boost. You don’t need to use the card — just being listed as an authorized user helps.

1–3 Years Post-Discharge

When You Can Get a Mortgage

FHA loans become available 2 years after Chapter 7 discharge (with re-established credit and debt-to-income ratio in good shape). Conventional loans through Fannie Mae: 4 years after Chapter 7 discharge. Many people who file bankruptcy in their 30s go on to buy homes before age 40 with this timeline.

Avoid These Rebuilding Mistakes

- Opening too many new accounts quickly — multiple hard inquiries hurt scores in the short term

- Carrying balances on credit cards — pay in full every month

- Financing a new car at a predatory rate immediately after discharge — wait 12–18 months for better rates

- Closing old accounts (if any survived bankruptcy) — length of credit history matters

Building a Different Financial Life

The practical skills that prevent the return to bankruptcy: zero-based budgeting (spending plan before the month starts), emergency fund as a non-negotiable priority, automated savings and debt payments, and a clear understanding of your “why” for financial stability. Most people who go through bankruptcy once emerge with significantly stronger financial literacy and habits than before — the experience changes how they relate to money.

FAQ

Can I get a credit card after Chapter 7?

Yes — secured cards are available immediately after discharge from most major issuers. Unsecured cards with reasonable terms become available within 12–24 months of consistent positive credit behavior. Capital One and Discover specifically have programs for bankruptcy recovery borrowers.

Should I pay to remove bankruptcy from my credit report?

No legitimate service can remove an accurate bankruptcy entry before its legal expiration date. “Credit repair” companies that promise to remove accurate negative items are typically scams. What legitimately improves your credit: correcting inaccurate items and building positive history through the steps above.