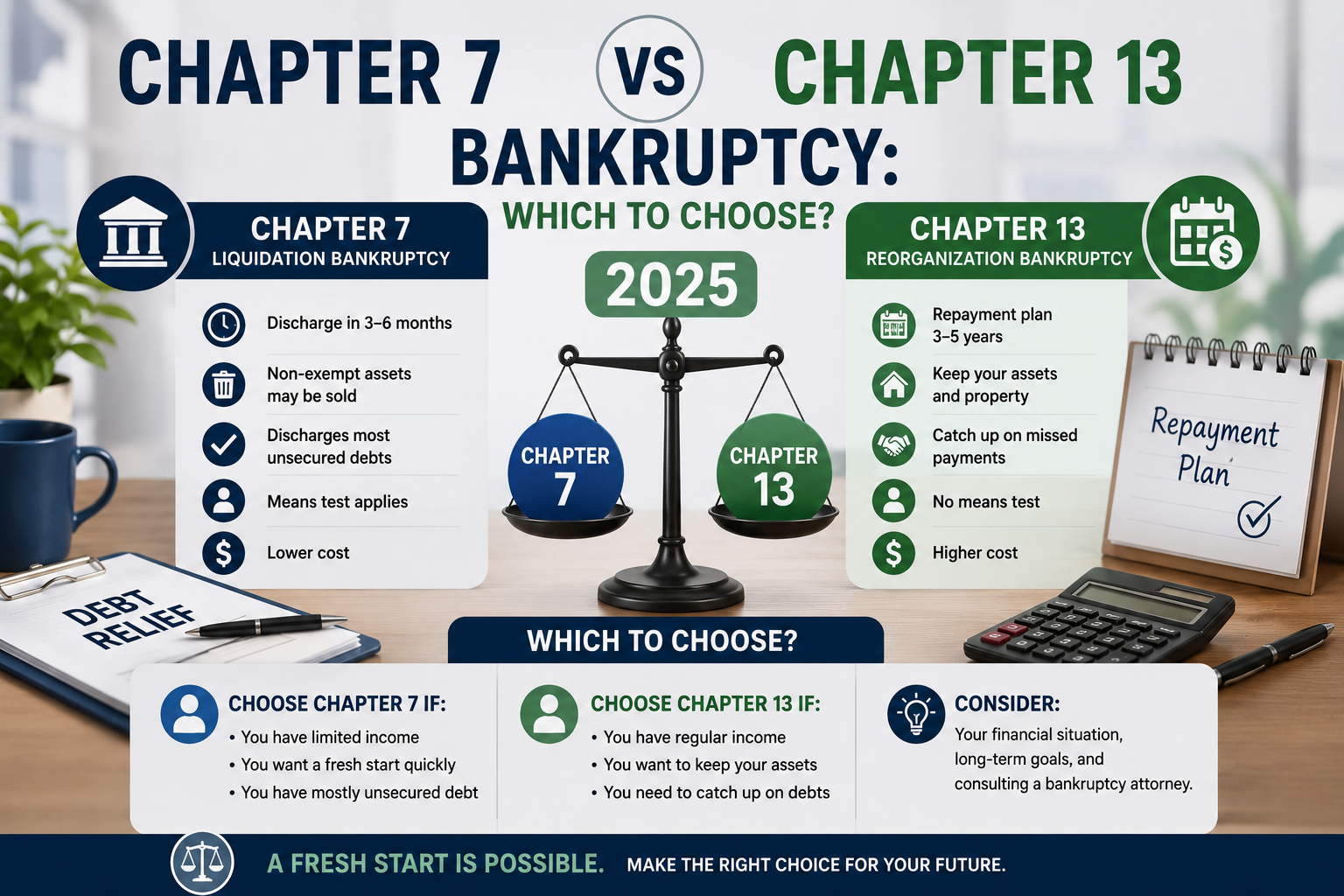

Chapter 7 vs Chapter 13 Bankruptcy: Which to Choose 2025

3–6 mo — Chapter 7 timeline from filing to full discharge of eligible debts

3–5 yrs — Chapter 13 repayment plan duration before discharge

70% — Personal bankruptcy filers who choose Chapter 7 — simpler and faster

7 yrs — Chapter 13 stays on credit report vs 10 years for Chapter 7

$338 — Chapter 7 filing fee vs $313 for Chapter 13 — both very affordable

The Core Difference in Plain Terms

Chapter 7 is liquidation bankruptcy — you wipe out eligible debts entirely in 3–6 months with no payments to creditors. Chapter 13 is reorganization bankruptcy — you keep your assets but repay some or all debts through a 3–5 year court-approved plan. Chapter 7 is faster and simpler; Chapter 13 offers protection for people with assets to protect or incomes too high for Chapter 7.

About 70% of personal bankruptcy filers choose Chapter 7. But Chapter 13 is the right choice for specific situations that Chapter 7 simply cannot address.

Side-by-Side Comparison

| Factor | Chapter 7 | Chapter 13 |

|---|---|---|

| Timeline | 3–6 months | 3–5 years |

| Debt outcome | Most unsecured debt discharged entirely | Repay some or all through approved plan |

| Income limit | Must pass means test (lower income) | Must have regular income for plan payments |

| Asset protection | Non-exempt assets may be liquidated | Keep all assets; pay equivalent value instead |

| Home in foreclosure | Temporary stop only — doesn’t cure arrears | Can cure mortgage arrears over the plan period |

| Credit report impact | 10 years from filing | 7 years from filing |

| Typical attorney fees | $1,000–$2,000 | $3,000–$4,500 |

When Chapter 7 Is the Better Choice

Choose Chapter 7 if: your income is below your state’s median income, you have mostly credit card and medical debt with few assets, you want to be debt-free as quickly as possible, and you don’t own a home in foreclosure that needs saving.

Example: Marcus earned $38,000/year (below Texas median of $58,100) and had $45,000 in credit card and medical debt. Renting, driving a car within the state exemption. Filed Chapter 7, discharged all $45,000 in 4 months, total cost $338.

When Chapter 13 Is the Better Choice

Choose Chapter 13 if: your income exceeds the means test limit; you’re behind on mortgage payments and want to save your home (Chapter 13 lets you catch up on arrears over 3–5 years); you have significant non-exempt assets; you have co-signers to protect (Chapter 13’s co-debtor stay protects co-signers; Chapter 7 does not); or you have priority debts like recent taxes or domestic support arrears you need to manage.

For step-by-step Chapter 7 filing: How to File Chapter 7 Bankruptcy Yourself | For income qualification: The Bankruptcy Means Test

Frequently Asked Questions

Can I convert from Chapter 13 to Chapter 7?

Yes — if your income drops during a Chapter 13 plan and you now pass the means test, file a Notice of Conversion with your bankruptcy court. This is a relatively common occurrence when people lose jobs mid-plan.

Does Chapter 13 save my house from foreclosure?

Yes — this is Chapter 13’s most powerful advantage over Chapter 7. The automatic stay stops foreclosure immediately, and your plan can include paying mortgage arrears over 3–5 years while continuing regular payments. You must complete the entire plan to make this protection permanent.

Which is better for my credit score long term?

Chapter 13 stays on your credit report for 7 years vs 10 years for Chapter 7 — a small technical advantage. However, Chapter 7’s faster resolution and clean slate sometimes allows quicker practical rebuilding. Individual results vary significantly.

Can I file Chapter 13 without a lawyer?

Technically yes, but far harder than Chapter 7. Chapter 13 requires drafting a court-confirmed repayment plan, attending a confirmation hearing, and managing 3–5 years of payment administration. Pro se Chapter 13 failure rates are significantly higher. At minimum, consult a bankruptcy attorney before filing Chapter 13.

What if I miss a Chapter 13 payment?

Missing payments can result in case dismissal, which removes bankruptcy protection and lets creditors resume collection immediately. Contact your trustee immediately if you cannot make a payment — plans can be modified in response to legitimate changed circumstances.

Can I eliminate a second mortgage in Chapter 13?

Yes — called ‘lien stripping.’ If your home is worth less than your first mortgage balance, the second mortgage can be reclassified as unsecured debt and potentially discharged through the plan. This is a major Chapter 13 advantage for homeowners who are underwater.

The Bottom Line

Chapter 7 wins on speed and simplicity. Chapter 13 wins on flexibility and asset protection. The choice isn’t about which is universally ‘better’ — it’s about which fits your specific financial situation right now. Use the comparison table above as your starting framework before making your decision.