How to Stop Wage Garnishment Immediately in 2026

Wage garnishment can take up to 25% of your disposable income from every paycheck — often with little advance warning. But garnishment is not unstoppable. This guide covers every legal method to stop it, from bankruptcy’s immediate automatic stay to court challenges and creditor negotiations.

How Wage Garnishment Works

Most creditors must sue you in court, obtain a judgment, then apply for a writ of garnishment before touching your wages. This process takes weeks to months — giving you time to act. Exceptions that skip court: IRS (tax debt), child support agencies, and federal student loan collectors can garnish without a judgment.

Federal Garnishment Limits

- Consumer debt (credit cards, medical bills): Lesser of 25% of disposable earnings OR the amount above 30 × federal minimum wage per week

- Child support/alimony: Up to 50–65% of disposable earnings

- Federal tax debt: Table-based, typically 70–90% after exemptions

- Student loans: Up to 15% of disposable earnings

Many states have more protective limits than federal law.

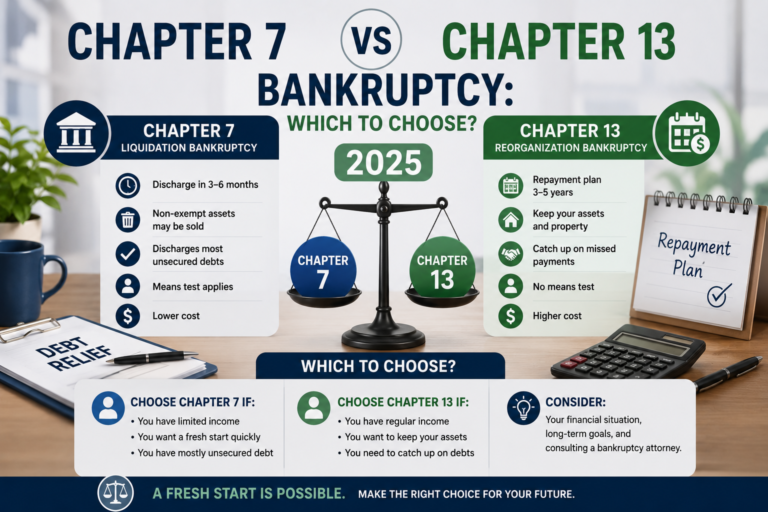

Method 1: File for Bankruptcy (Most Complete)

Filing bankruptcy triggers the automatic stay — an immediate, court-ordered halt to ALL collection including wage garnishment. The moment your bankruptcy case is filed (before your first court date), the garnishment must stop. After filing, call your HR/payroll department immediately and provide your case number — don’t wait for official court notice. For the full filing process, see our guide on how to file Chapter 7 yourself.

Method 2: Challenge the Judgment in Court

Within your state’s challenge window (often 30 days from judgment), you can contest the garnishment if: the debt isn’t yours, you weren’t properly served the lawsuit, the debt is past the statute of limitations, the amount is wrong, or the garnishment exceeds legal limits.

Method 3: Claim an Exemption

Certain income is completely exempt from garnishment:

- Social Security benefits (protected from most creditor garnishment)

- Disability benefits (SSDI, SSI) — fully protected

- Veterans’ benefits — fully protected

- Pension and retirement benefits while in the account

If protected income is being garnished, file a claim of exemption immediately with the issuing court.

Method 4: Negotiate With the Creditor

Once a creditor has a judgment, they have leverage — but so do you (you can file bankruptcy and potentially discharge the debt entirely). Call the creditor’s attorney and offer a realistic payment plan. Many will suspend garnishment pending plan compliance. Get any agreement in writing before it takes effect.

Method 5: Request a Hardship Hearing

If garnishment leaves you unable to pay essential living expenses, file a claim of exemption or request a court hearing to reduce the garnishment amount. Document your income and essential expenses. Courts have discretion to reduce garnishment in genuine hardship cases.

Child Support and Tax Garnishment

Child support: Bankruptcy’s automatic stay does NOT stop child support garnishments. Negotiate directly with the family court or state agency for a modified order.

IRS garnishment: The automatic stay does stop IRS garnishments, though the tax debt itself may not be dischargeable depending on age and other factors.

FAQ

How quickly does bankruptcy stop garnishment?

The automatic stay is legally effective the moment your petition is filed. However, to actually stop a payroll deduction you must notify your employer directly — fax or email your case number to payroll immediately. Most employers stop deductions in the next pay cycle after receiving notice.

Can I recover money already garnished?

Generally no, for consumer debt garnished before your filing. Amounts taken within 90 days before filing may be recoverable as “preferential transfers” by the bankruptcy trustee — but that’s a trustee action, not one you control.

Stop Your Wage Garnishment Today

Free checklist — fastest legal paths to stopping garnishment in your state.